Introduction

In an increasingly complex financial and regulatory environment, ensuring that companies can meet their future obligations is critical. One important evaluation method used by insurers and financial institutions is the liability adequacy test in USA 2026. This test plays a key role in assessing whether an organization’s recorded liabilities are sufficient to cover expected future claims and obligations. As regulatory standards evolve in 2026, understanding how this test works and why it matters has become essential for insurers, auditors, regulators, and financial professionals.

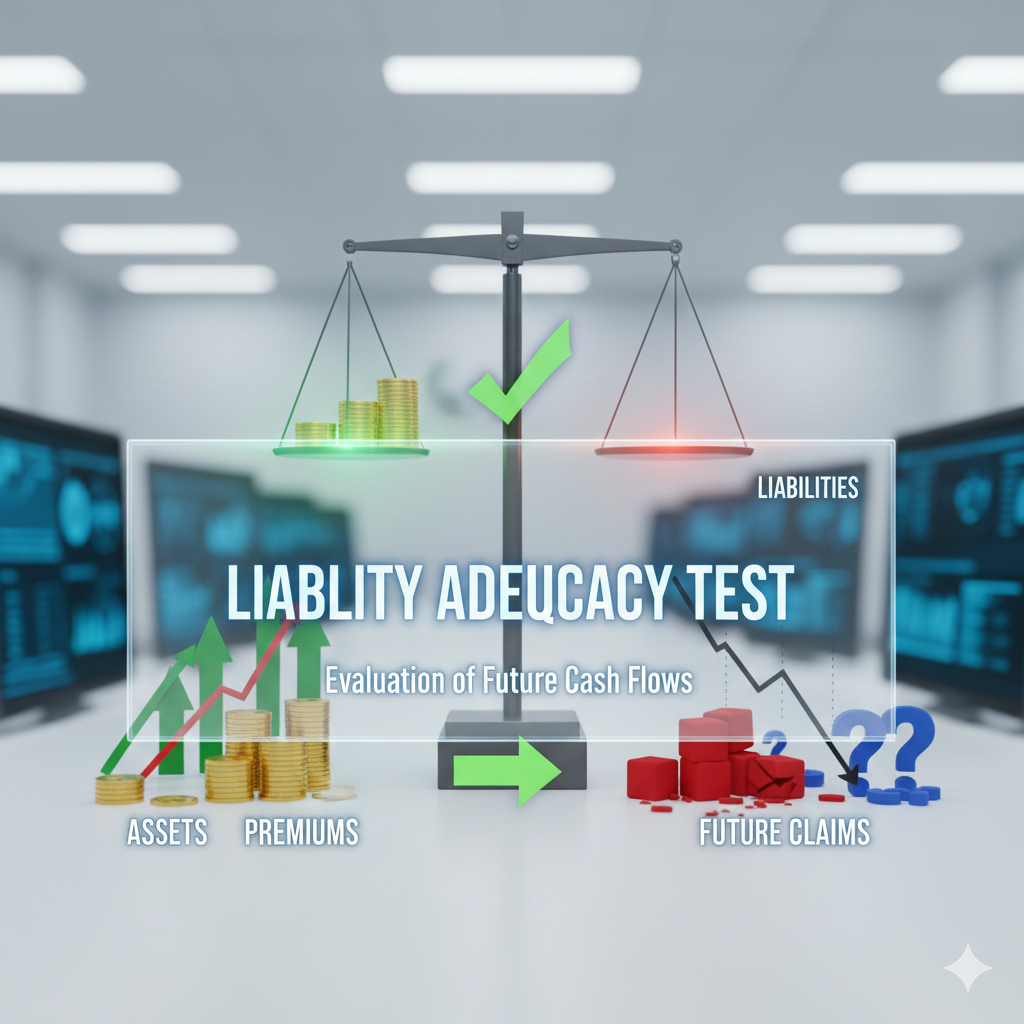

What Is a Liability Adequacy Test?

A liability adequacy test (LAT) is a financial assessment used primarily in the insurance industry to determine whether existing liability reserves are adequate. The test compares the carrying amount of liabilities on a company’s balance sheet with the present value of expected future cash outflows related to insurance contracts or other long-term obligations.

If the test reveals that liabilities are understated, the company must recognize an additional expense and increase its reserves. This ensures financial statements present a realistic view of the company’s financial health.

Purpose of Liability Adequacy Test in USA 2026

The liability adequacy test in USA 2026 serves several critical purposes:

- Protects policyholders by ensuring insurers can meet future claims

- Enhances transparency and accuracy in financial reporting

- Supports regulatory compliance and risk management

- Prevents under-reserving, which could lead to insolvency

With economic uncertainty, inflation, and changing actuarial assumptions in 2026, liability adequacy testing has become even more important.

Who Must Perform Liability Adequacy Tests?

Liability Adequacy Tests (LAT) must be performed by insurance companies to ensure their recognized liabilities for future claims are sufficient, a requirement under IFRS standards (IFRS 4 and the newer IFRS 17) to confirm they can meet policyholder obligations, involving detailed actuarial analysis of future cash flows, and are often done annually. While primarily for insurers, the principle applies to any entity with significant long-term financial commitments or risk, but the formal mandated test is for the insurance sector.

Regulators such as state insurance departments and standard-setting bodies expect regular and well-documented testing.

Regulatory Framework in USA 2026

The liability adequacy test in USA 2026 is guided primarily by U.S. Generally Accepted Accounting Principles (GAAP) and statutory accounting practices. Insurance regulators also follow guidance from organizations such as the National Association of Insurance Commissioners (NAIC).

Key regulatory expectations include:

- Use of realistic and updated assumptions

- Consideration of interest rates, mortality, morbidity, and lapse rates

- Inclusion of all future policy-related expenses and benefits

- Clear documentation and disclosure of test results

In 2026, regulators are emphasizing stress testing and scenario analysis to account for economic volatility.

How the Liability Adequacy Test Works

The liability adequacy test generally follows these steps:

- Identify Relevant Liabilities

Insurance contract liabilities or long-term obligations are grouped for testing. - Estimate Future Cash Flows

Actuaries project future claims, benefits, and related expenses. - Discount Cash Flows

Expected cash flows are discounted using appropriate interest rates. - Compare With Booked Liabilities

The present value of expected cash flows is compared to existing reserves. - Recognize Deficiencies

If liabilities are insufficient, additional reserves must be recorded immediately.

This process ensures that financial statements remain conservative and reliable.

Key Assumptions Used in Liability Adequacy Testing

The accuracy of the liability adequacy test in USA 2026 depends heavily on assumptions, including:

- Interest and discount rates

- Policyholder behavior (lapses, renewals)

- Mortality and morbidity trends

- Inflation and healthcare cost growth

- Claims frequency and severity

Small changes in assumptions can significantly affect results, making professional judgment critical.

Challenges in 2026

Several challenges impact liability adequacy testing in 2026:

- Rising inflation, increasing claim costs

- Interest rate volatility, affecting discount rates

- Climate-related risks, influencing insurance claims

- Data quality and modeling complexity

Insurers must continuously update models to reflect current market and economic conditions.

Impact on Financial Statements

When a liability adequacy test identifies a deficiency, the company must:

- Increase insurance liabilities

- Recognize an immediate expense

- Reduce net income for the reporting period

Although this may negatively affect short-term earnings, it strengthens long-term financial stability and credibility.

Importance for Stakeholders

The liability adequacy test in USA 2026 is valuable to multiple stakeholders:

- Policyholders gain confidence in insurer solvency

- Investors receive more accurate financial information

- Regulators ensure compliance and risk management

- Auditors rely on LAT results for financial reviews

It serves as a cornerstone of prudent financial oversight.

Conclusion

The liability adequacy test in USA 2026 remains a vital financial safeguard, ensuring that insurers and financial institutions maintain sufficient reserves to meet future obligations. With evolving regulations, economic uncertainty, and growing risk exposure, this test plays a crucial role in promoting transparency, stability, and consumer protection. Organizations that perform thorough and well-documented liability adequacy testing are better positioned to withstand financial stress and maintain regulatory compliance in 2026 and beyond.

Leave a Reply